Public vs Private Foundation in Canada: Key Differences

Published on

October 24, 2021

Last updated on

March 2, 2026

When establishing a charitable organization in Canada, understanding the difference between a public foundation and a private foundation is crucial. Both must be set up as corporations or trusts and registered with the Canada Revenue Agency (CRA) to obtain tax-exempt status. However, their governance, funding sources, and operational rules differ significantly.

What Is a Foundation?

A foundation is a type of charity that provides funding or services to support charitable causes. Foundations can either:

- Distribute funds to other charities (grant-making).

- Run their own charitable programs.

What Does a Foundation Do?

Foundations play a vital role in philanthropy by:

- Supporting other nonprofits through grants.

- Funding research, education, and social programs.

- Managing endowments to ensure long-term charitable impact.

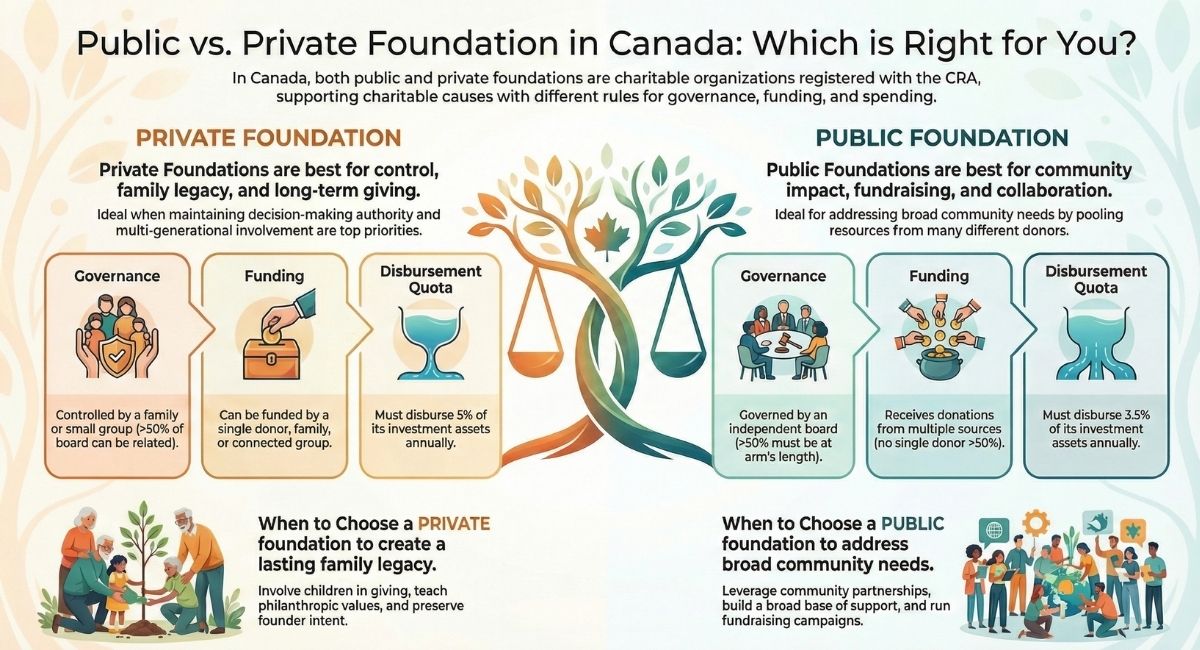

Public Foundation vs. Private Foundation: Key Differences

Public Foundation

- Governance: More than 50% of the board members must be independent (at arm’s length).

- Funding: Receives donations from multiple sources; no single donor can contribute more than 50% of funding.

- Disbursement Requirements: Must allocate over 50% of annual funds to other qualified charities.

Private Foundation

- Governance: Typically controlled by a single family or small group; more than 50% of board members may be related or not at arm’s length.

- Funding: Can receive most (or all) of its funding from a single donor, family, or closely connected group.

- Flexibility: Can either fund other charities or run its own charitable programs.

Private Foundation Rules in Canada

If you’re considering setting up a private foundation, it’s important to understand the regulations:

- Must meet annual disbursement quota (currently 3.5% of investment assets).

- Subject to stricter compliance rules than public foundations.

- Donations receive tax benefits, making them attractive for high-net-worth individuals.

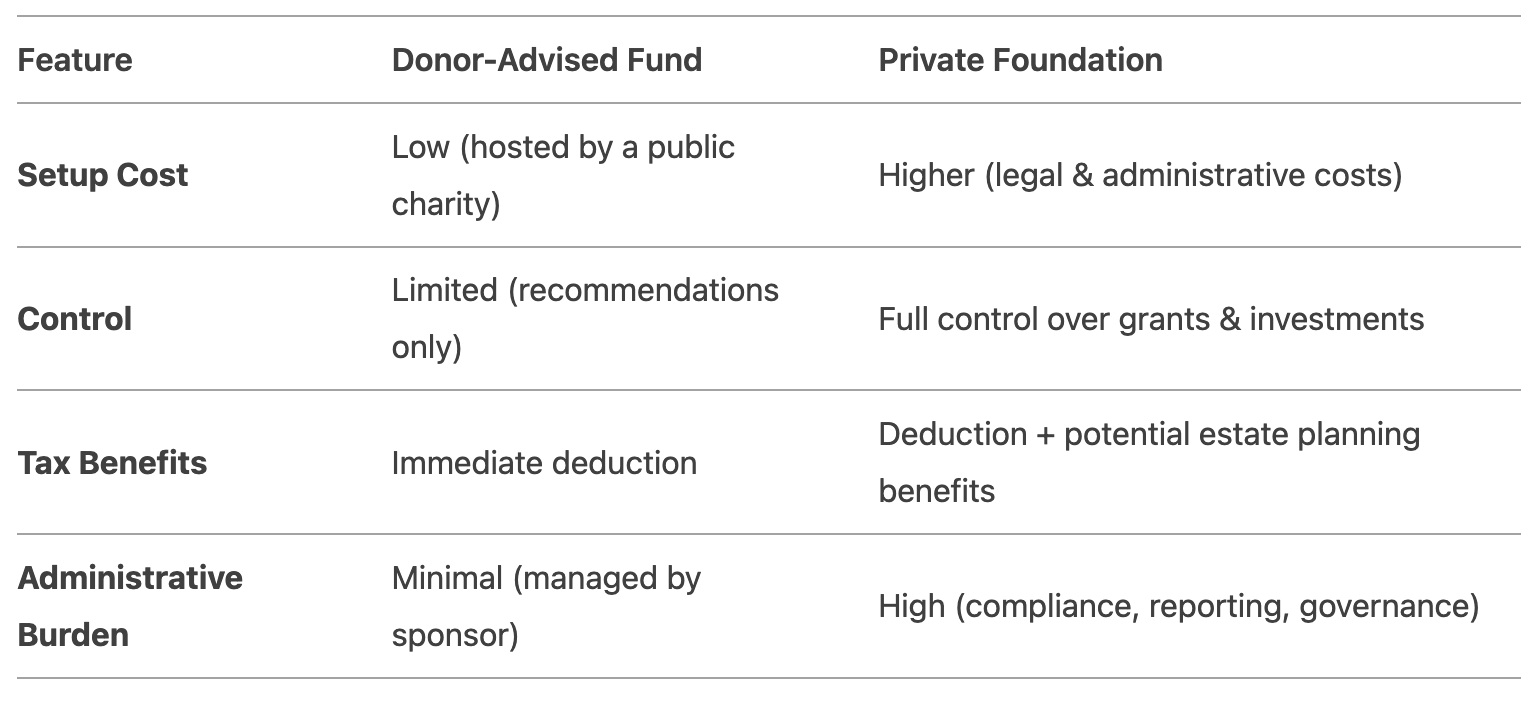

Which Is Better: A Donor-Advised Fund or a Private Foundation?

Many donors debate whether to use a donor-advised fund (DAF) or register a private foundation. Here’s a quick comparison:

A private foundation is ideal for those who want full control and long-term family involvement, while a donor-advised fund offers simplicity and lower costs.

What Is a Private Foundation for Tax Purposes?

For tax purposes, a private foundation is a registered charity with specific CRA rules:

- Tax receipts can be issued for donations.

- Subject to penalties if disbursement quotas are not met.

- Investment income is tax-exempt if used for charitable purposes.

When to Choose a Private Foundation in Canada

Private foundations work best in specific scenarios where donor control and family involvement are priorities.

Family Philanthropy Scenarios

Consider a private foundation when:

- Multiple family members want to engage in philanthropy together

- You want to create a vehicle for teaching philanthropic values across generations

- Family members have complementary charitable interests and approaches

- You seek to create a shared legacy reflecting family values

- You want to involve children and grandchildren in giving decisions

- The foundation can serve as a unifying force for family members

Many families find that private foundations strengthen family bonds while making a meaningful impact.

Long-term Giving Strategies

Private foundations excel for:

- Creating a permanent endowment to support causes indefinitely

- Implementing sophisticated, multi-year funding strategies

- Supporting causes that require patient, long-term funding

- Building expertise in specific charitable niches

- Developing deep relationships with grantee organizations

- Creating sustainable support for organizations beyond a donor's lifetime

The ability to take a long view makes private foundations powerful vehicles for strategic philanthropy.

Legacy Planning Considerations

Choose a private foundation when legacy matters:

- You want to create a lasting philanthropic monument to family values

- You seek to establish a named foundation that will endure for generations

- You wish to institutionalize specific charitable priorities

- You want to influence certain fields or issues beyond your lifetime

- You aim to involve family members in philanthropy even after you're gone

- You desire to leave a structured, managed charitable vehicle rather than a simple bequest

A private foundation can be a powerful legacy planning tool when properly structured.

Control and Succession Preferences

Private foundations are ideal when:

- Maintaining decision-making authority is a top priority

- You have strong convictions about how charitable dollars should be spent

- You want to handpick successors who will carry forward your vision

- You prefer a small, carefully selected board of directors

- You want final say over investment philosophy and grant recipients

- You wish to preserve founder intent through governing documents

If control matters greatly, a private foundation likely offers the best structure.

If you’re considering setting up a private foundation and want a clearer picture of the steps involved, check out this helpful video guide on how to start a private foundation in Canada.

When to Choose a Public Foundation in Canada

Public foundations shine in situations requiring community engagement, fundraising capacity, and collaborative approaches.

Community Impact Goals

Public foundations work best when:

- Your focus is on addressing broad community needs

- You want to tap into collective community knowledge

- You aim to bring diverse stakeholders together around common causes

- You seek to leverage other community resources and partnerships

- You want to respond nimbly to emerging community issues

- You value inclusive decision-making with community input

Community foundations exemplify this approach by pooling community resources to address local needs.

Fundraising-focused Missions

Choose a public foundation if:

- Ongoing fundraising will be central to your charitable model

- You plan to actively solicit donations from many unrelated donors

- You need to build a broad base of financial support

- You want to offer donor-advised funds or other giving vehicles

- You seek to attract corporate or government funding

- You aim to grow your charitable capital beyond the founder's contribution

Public foundations can build substantial resources through effective fundraising strategies.

Collaborative Philanthropy Models

Public foundations excel for:

- Bringing multiple donors together around shared causes

- Creating collective impact through coordinated funding

- Building cross-sector partnerships with government and business

- Leveraging diverse expertise in grant-making decisions

- Addressing complex social issues requiring multiple stakeholders

- Sharing knowledge and resources across organizations

This collaborative approach can create impact beyond what any single donor could achieve.

Broader Governance Preferences

Public foundations are ideal when:

- You value diverse perspectives in charitable decision-making

- You want to engage community leaders in governance

- You prefer to separate personal relationships from foundation governance

- You benefit from specialized expertise beyond family members

- You value systems of checks and balances in charitable giving

- You see advantage in broader networks and connections

Diverse governance often leads to more robust decision-making and community connections.

Legal and Tax Implications of Each Foundation Structure

Both foundation types face specific legal and tax considerations that affect their operations.

Disbursement Quota Requirements

The disbursement quota creates different spending obligations:

- Private foundations must generally disburse 5% of their investment assets annually

- Public foundations must disburse at least 3.5% of their investment assets annually

- Failure to meet disbursement quotas can result in penalties or revocation

- Excess disbursements in one year can be carried forward to help meet future quotas

- Certain expenditures qualify toward the quota while others don't

- Applications can be made for relief from the disbursement quota in exceptional circumstances

Plan your grant-making strategy with these requirements in mind. For more on charity registration, check out our Complete Guide to Canadian Charity Registration.

Investment Restrictions

Investment rules seek to ensure prudent management:

- All foundations must invest assets in a manner consistent with prudent investment standards

- Foundations cannot make investments primarily to benefit related parties

- Private foundations face more scrutiny on investment choices

- Public foundations have somewhat more flexibility but still face restrictions

- Significant penalties can apply for non-compliance with investment rules

- Professional investment management is advisable for both foundation types

Develop a clear investment policy that complies with applicable restrictions.

Related Party Transaction Rules

Rules governing transactions with related parties differ:

- Private foundations face stricter limitations on transactions with related parties

- Public foundations have more flexibility but still must ensure transactions benefit the charity

- Both must avoid conferring undue benefits on related individuals or organizations

- Documentation and fair market value assessments are crucial for any related party transactions

- Non-compliance can lead to serious penalties for both the foundation and the related parties

- Careful governance procedures should be established for any potential related party interactions

Robust policies and documentation are essential, especially for private foundations.

Director Liability Considerations

Directors of both foundation types face significant responsibilities:

- Directors have fiduciary duties to the foundation

- Personal liability can arise for certain compliance failures

- Private foundations directors often face higher scrutiny due to related party concerns

- Public foundations directors must oversee more complex fundraising and program operations

- Insurance and indemnification provisions are important for both

- Regular governance training helps directors understand their obligations

Ensure directors understand their legal duties and provide appropriate liability protection.

Converting Between Foundation Types in Canada

Sometimes, organizations need to change their foundation status as circumstances evolve.

Process for Changing Status

Conversion requires a formal process:

- Board resolution approving the change

- Amendment of governing documents to reflect new status requirements

- Changes to board composition if needed (particularly for private to public conversion)

- Submission of documentation to CRA requesting redesignation

- CRA review and approval process

- Implementation of new governance and operational procedures

This process typically takes several months and requires careful planning.

Potential Challenges and Considerations

Conversion brings several challenges:

- Private to public conversion requires diversifying the board and funding sources

- Public to private conversion may require consolidating control and addressing ongoing fundraising expectations

- Both directions require policy and procedure updates

- Stakeholder communication is essential, especially for public foundations

- Investment and grant-making strategies may need adjustment

- Organizational identity and culture shifts may be difficult

Careful change management helps navigate these challenges successfully.

Timeline and Costs

The conversion process involves:

- 3-6 months for typical conversions (sometimes longer)

- Legal fees for document amendments and CRA submissions

- Potential costs for board recruitment and training

- Communication expenses with stakeholders

- Possible consulting fees for restructuring assistance

- Ongoing compliance costs in the new structure

Budget appropriately for these expenses when planning a conversion.

Case Studies: Successful Canadian Foundations

Real-world examples illustrate effective foundation strategies.

Examples of Well-structured Private Foundations

Several private foundations demonstrate best practices:

- The Lucie and André Chagnon Foundation: Established by the founder of Vidéotron, this family foundation focuses on educational success and poverty prevention in Quebec, demonstrating effective governance while maintaining family control.

- The Sprott Foundation: Founded by resource investor Eric Sprott, this foundation maintains a focused approach to tackling homelessness and hunger in Canada through strategic partnerships with frontline organizations.

- The Azrieli Foundation: This family foundation excels at multi-generational involvement while supporting education, architectural initiatives, and scientific research in both Canada and Israel.

These foundations maintain strong family involvement while creating significant impact in their chosen fields.

Examples of Effective Public Foundations

Successful public foundations include:

- Vancouver Foundation: Canada's largest community foundation effectively pools resources from thousands of donors to address local needs while offering donor-advised funds and specialized programs.

- The Mastercard Foundation: Though initially founded with corporate funding, this foundation has evolved into a public foundation with diverse governance and partners to advance education and financial inclusion globally.

- The Ontario Trillium Foundation: This public foundation effectively distributes government and lottery proceeds to strengthen community organizations across Ontario through collaborative grant-making processes.

These foundations demonstrate the power of collaborative approaches and diverse funding sources.

Lessons Learned from Each Model

Key lessons emerge from successful foundations:

- Clear mission focus correlates strongly with impact

- Strong governance structures prevent mission drift

- Professional management enhances effectiveness

- Transparent operations build public trust

- Deliberate succession planning ensures continuity

- Strategic collaboration amplifies impact

- Regular evaluation improves outcomes

- Attention to compliance prevents regulatory issues

Apply these lessons regardless of which foundation type you choose.

Need Help Setting Up a Foundation?

Whether you’re exploring a public foundation, a private foundation, or a donor-advised fund, our experienced Foundation Lawyers can guide you through the process.

Call us at 416-488-5888

Email: ask@charitylawgroup.ca

Let us help you establish your foundation on solid legal footing while maximizing tax benefits and philanthropic impact.

Frequently Asked Questions

What is the difference between a public and private foundation in Canada?

A public foundation receives donations from multiple unrelated donors (no single donor over 50%) and must have more than 50% independent board members. A private foundation can be funded entirely by one donor or family, with more than 50% of board members being family or related parties. Private foundations face a 5% annual disbursement quota compared to 3.5% for public foundations and stricter CRA compliance rules.

How does the Canada Revenue Agency (CRA) define public vs private foundations?

CRA classifies a foundation as "public" if more than 50% of its directors are at arm's length from each other AND no more than 50% of its capital comes from one person or related group. If a foundation doesn't meet both criteria, it's designated as a private foundation. This classification determines disbursement quotas, related party transaction restrictions, and compliance requirements.

Which type of foundation is better for a family that wants control?

A private foundation is ideal for families seeking control. It allows more than 50% of board members to be family members, letting you maintain decision-making authority across generations. You choose which charities receive funding, set grant-making priorities, and pass control to chosen successors. The tradeoff is higher costs and stricter CRA compliance rules.

Which type of foundation is better for community-based fundraising?

Public foundations excel at community-based fundraising because independent governance builds donor trust. They can offer donor-advised funds, host events, launch capital campaigns, and attract government or corporate funding more easily. Community foundations demonstrate this by raising millions from thousands of donors, though this requires investment in fundraising staff and donor relations.

Do public and private foundations in Canada follow different operating rules?

Yes. Private foundations must disburse 5% of investment assets annually versus 3.5% for public foundations. Private foundations face stricter rules on related party transactions—they generally cannot pay family members or make investments benefiting relatives. Public foundations have more flexibility but must maintain independent boards and demonstrate diverse funding sources.

The material provided on this website is for information purposes only.. You should not act or abstain from acting based upon such information without first consulting a Charity Lawyer. We do not warrant the accuracy or completeness of any information on this site. E-mail contact with anyone at B.I.G. Charity Law Group Professional Corporation is not intended to create, and receipt will not constitute, a solicitor-client relationship. Solicitor client relationship will only be created after we have reviewed your case or particulars, decided to accept your case and entered into a written retainer agreement or retainer letter with you.

DOV GOLDBERG, J.D. is a lawyer at B.I.G. Charity Law Group and has dedicated his career exclusively to Charity and Not-for-Profit Law for over a decade. Dov guides charities, foundations, and non-profit organizations through every stage of the registration process, offering practical legal advice with a focus on compliance, governance, and long-term success. Known for his hands-on approach and deep knowledge of CRA requirements, Dov is committed to helping clients build strong, sustainable, and legally sound organizations.

Tax Return for Revoked Charity Form

.png)