What is a Charitable Purpose?

Published on

July 21, 2023

Last updated on

March 17, 2026

If you are starting a charity or nonprofit in Canada, one of the first questions the CRA will ask is: what is your charitable purpose? Getting this right is not optional — it is the foundation of your entire registration application.

The legal interpretation of "charity" in Canada has evolved through centuries of common law, shaped by court decisions and CRA guidance. As of 2026, the CRA continues to apply the four-heads framework — originally established in the landmark 1891 case of Pemsel v. Special Commissioners of Income Tax — alongside a two-part public benefit test when reviewing charitable registration applications.

This framework applies to all registered charities and also to charitable trusts, regardless of registration status. A valid charitable trust must be established with the intention of serving a charitable purpose.

Understanding what qualifies — and what does not — can save your organization months of delays or a refused application.

What is a Charitable Purpose in Canada?

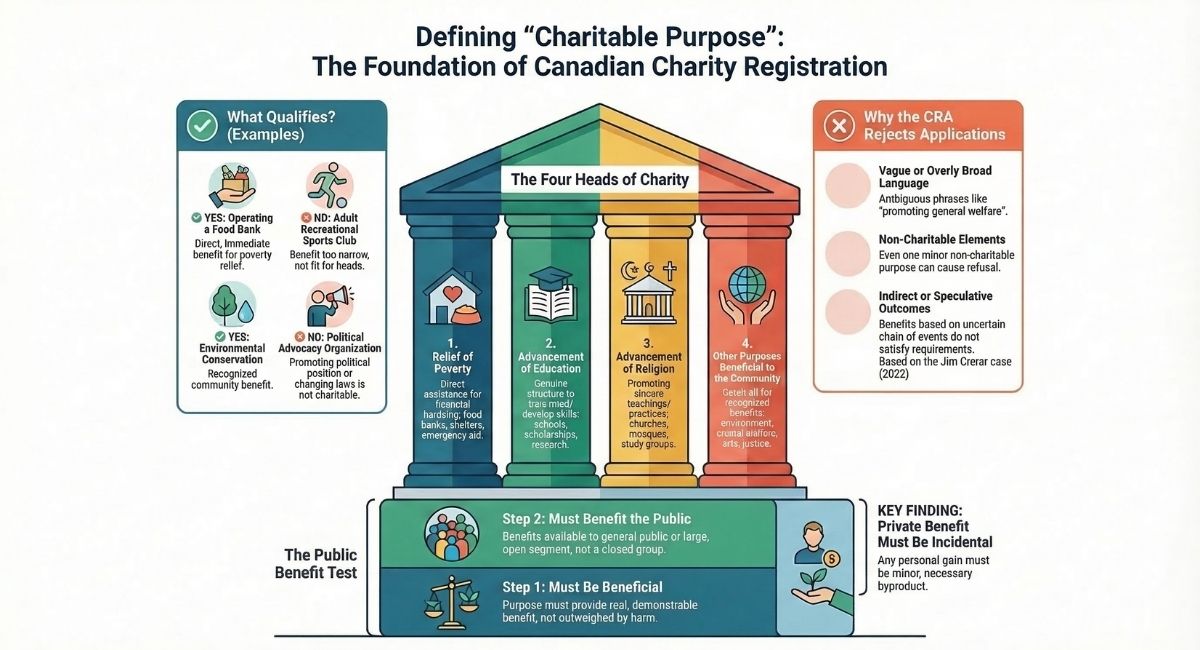

A charitable purpose is a purpose that falls under one of four legal categories recognized under Canadian charity law: relief of poverty, advancement of education, advancement of religion, or other purposes that benefit the community. To qualify, the purpose must also pass the public benefit test — meaning it must benefit the public, or a substantial segment of it, in a way that is clearly and demonstrably beneficial. The Canada Revenue Agency (CRA) uses these criteria when assessing whether an organization qualifies for charitable registration in Canada.

The Four Heads of Charity in Canada

The foundation for determining what counts as a charitable purpose in Canada comes from Pemsel v. Special Commissioners of Income Tax (1891), a landmark ruling that defined four categories — known as the "four heads of charity." Canadian courts and the CRA continue to rely on this framework today.

1. Relief of Poverty

This head covers purposes that directly help individuals or groups living in poverty or financial hardship. The CRA interprets relief of poverty broadly — it does not require destitution. An organization qualifies if its purpose is to provide real, immediate relief to those who are in need.

Canadian examples:

- Food banks and meal programmes

- Emergency financial assistance

- Shelters and transitional housing

- Clothing and essential goods distribution

Important: The CRA looks for direct, immediate relief. Purposes that only indirectly address poverty — or that rely on uncertain outcomes — are unlikely to qualify. The Jim Crerar Charitable Trust case (discussed below) is a clear illustration of this.

2. Advancement of Education

This head covers purposes that train the mind, develop skills, or contribute to the body of knowledge. Simply sharing information is not enough — the purpose must have genuine educational value and structure.

Canadian examples:

- Schools, colleges, and universities

- Scholarship and bursary programmes

- Literacy and numeracy organizations

- Vocational training and skills development

- Research organizations that publish and disseminate findings

Important: Entertainment or activities that provide personal enrichment without clear educational methodology will not qualify under this head.

3. Advancement of Religion

This head covers purposes that promote a religion — its teachings, practice, and spiritual welfare of its followers. The religion must be sincere and must not be contrary to public policy or morality.

Canadian examples:

- Churches, mosques, temples, synagogues, and gurdwaras

- Religious study organizations

- Organizations that publish and distribute religious materials

Important: An organization that promotes a specific religion qualifies. One that promotes "spirituality" in a vague or secular sense may face scrutiny.

4. Other Purposes Beneficial to the Community

This is the broadest and most complex head. It serves as a catch-all category for purposes that do not fit neatly into the first three heads but are still recognized as genuinely charitable.

To qualify under this head, a purpose must:

- Be analogous to the spirit and intention of the Statute of Elizabeth (1601)

- Benefit a substantial segment of the public — not a private or closed group

- Provide a benefit that is clearly recognized as charitable under the law

Purposes recognized by CRA and Canadian courts:

- Protection and preservation of the environment

- Promotion of the arts and culture

- Advancement of animal welfare (humane societies)

- Promotion of health and wellness

- Providing access to justice for those who cannot afford it

Purposes that have NOT qualified:

- Adult recreational sports clubs (benefit too narrow)

- Mutual benefit or members-only organizations

- Fraternal societies where the primary benefit is to members

Summary Table: The Four Heads of Charity

The Public Benefit Test

Being able to identify which head of charity your purpose falls under is only part of the equation. The CRA also applies a two-part public benefit test to every charitable purpose.

To pass this test, a purpose must:

1. Be beneficial. The benefit must be real, demonstrable, and not outweighed by harm. A purpose that causes harm to the public — even if well-intentioned — will not qualify.

2. Benefit the public. The benefit must extend to the public or to a sufficiently large and open segment of it. A purpose that primarily benefits a private group, a closed membership, or a narrow class of individuals will not meet this requirement.

This is why sports clubs, fraternal organizations, and mutual benefit societies generally cannot register as charities in Canada. Even if their activities are positive, the benefit flows primarily to members rather than to the public at large.

The CRA's guidance documents — including CG-013 (Charitable Purposes) and CG-027 (Public Benefit) — provide detailed direction on how this test is applied in practice.

Private benefit must be incidental. If your organization's activities create any private benefit — for example, financial gain for a founder or director — that benefit must be incidental and not the primary outcome of the purpose.

What Qualifies as a Charitable Purpose in Canada? (2026 Examples)

How Does the CRA Determine If a Purpose Is Charitable?

When you apply to register a charity in Canada, the CRA reviews your governing documents — your letters patent, articles of incorporation, or constitution — to assess whether your stated purposes are charitable.

Here is what the CRA looks for:

Your purposes must be exclusively charitable. Even one non-charitable purpose in your governing documents can result in a refused application. The CRA takes an all-or-nothing approach to this requirement.

Your purposes must be clear and specific. Vague, overly broad, or ambiguous language is one of the most common reasons applications are delayed or refused. Stating that your organization exists "to promote the general welfare of the community" is not sufficient.

Your activities must match your purposes. The CRA reviews both your stated purposes and your proposed activities. If your activities do not align with your charitable purposes, your application will face scrutiny.

Your purposes must benefit the public. Private benefit — even as a secondary outcome — can disqualify your application if it is not truly incidental to your charitable purpose.

Common Reasons CRA Rejects a Charitable Purpose

- The purpose is too vague or undefined

- The purpose includes a non-charitable element (even a minor one)

- The benefit is private rather than public

- The purpose is political or involves advocacy for a political position

- The proposed activities do not align with the stated purpose

- The purpose relies on indirect or speculative outcomes to generate a benefit

If you are unsure whether your purposes will pass CRA review, working with a charity lawyer before submitting your application can prevent costly delays.

A Recent Canadian Decision: Jim Crerar Charitable Trust (Re), 2022

The Jim Crerar Charitable Trust (Re), 2022 remains one of the most instructive recent Canadian decisions on what courts expect from a charitable purpose. Decided by the British Columbia Supreme Court, it provides a clear illustration of how strictly the courts apply both the four-heads framework and the public benefit test.

(Keep all the existing content for this section as-is — Relief of Poverty analysis, Purpose Beneficial to the Community analysis, and the commentary paragraph)

Key Takeaway from the Crerar Case

Charitable purposes must deliver direct, identifiable public benefit. Indirect or speculative outcomes — even well-intentioned ones — are unlikely to satisfy CRA or the courts. If your purpose depends on an uncertain chain of events to produce a benefit, it may not qualify as charitable.

Not sure if your organization's purpose qualifies as charitable?

Charitable purpose is one of the most technical — and most consequential — parts of a charity registration application. Getting it wrong can mean months of delays, a refused application, or problems down the road.

B.I.G. Charity Law Group works exclusively with charities and nonprofits across Canada. Dov Goldberg and his team can review your proposed purposes, help you structure your governing documents, and make sure your application gives you the best possible chance of approval.

📧 dov.goldberg@charitylawgroup.ca 📞 416-488-5888 🌐 CharityLawGroup.ca 📅 Book a free consultation

Frequently Asked Questions: Charitable Purposes in Canada

What are the four heads of charity in Canada?

The four heads of charity are: relief of poverty, advancement of education, advancement of religion, and other purposes beneficial to the community. These categories were established in the 1891 Pemsel case and continue to form the basis of Canadian charity law as of 2026.

Does my organization's purpose need to be exclusively charitable?

Yes. Under Canadian charity law, a registered charity must operate exclusively for charitable purposes. Even one non-charitable purpose — no matter how minor — can result in a refused registration application or a revocation of an existing registration.

Can a nonprofit have a charitable purpose without being a registered charity?

Yes. A nonprofit organization can pursue charitable purposes without being registered with the CRA. However, only registered charities can issue official donation receipts for income tax purposes and access the significant tax advantages that come with registered status.

What is the public benefit test for charities in Canada?

The public benefit test requires that a charitable purpose (1) produce a real and demonstrable benefit, and (2) deliver that benefit to the public or a sufficiently large and open segment of it. A purpose that primarily benefits a private group or closed membership will not pass this test.

Can advocacy or political activities be a charitable purpose in Canada?

No. Under Canadian charity law, purposes that are primarily political — including advocating for a change in law or government policy — are not considered charitable. Registered charities may engage in limited non-partisan public policy dialogue, but this cannot be their primary purpose.

What happens if the CRA determines my purpose is not charitable?

If you are applying to register, your application will be refused and you will receive a notice of intention to refuse with reasons. If you are already registered and your purposes are found to be non-charitable, your registration may be revoked, which means you lose the ability to issue donation receipts and must comply with distribution rules for your remaining assets.

Can I amend my charitable purposes after registration?

Yes, but you must notify the CRA of any changes to your governing documents, including amendments to your purposes. The CRA must approve the amended purposes to confirm they remain exclusively charitable. Failing to notify the CRA of changes can put your registration at risk.

The material provided on this website is for information purposes only.. You should not act or abstain from acting based upon such information without first consulting a Charity Lawyer. We do not warrant the accuracy or completeness of any information on this site. E-mail contact with anyone at B.I.G. Charity Law Group Professional Corporation is not intended to create, and receipt will not constitute, a solicitor-client relationship. Solicitor client relationship will only be created after we have reviewed your case or particulars, decided to accept your case and entered into a written retainer agreement or retainer letter with you.

DOV GOLDBERG, J.D. is a lawyer at B.I.G. Charity Law Group and has dedicated his career exclusively to Charity and Not-for-Profit Law for over a decade. Dov guides charities, foundations, and non-profit organizations through every stage of the registration process, offering practical legal advice with a focus on compliance, governance, and long-term success. Known for his hands-on approach and deep knowledge of CRA requirements, Dov is committed to helping clients build strong, sustainable, and legally sound organizations.

.png)