School Tuition Fees as Charitable Donations in Canada

Published on

March 19, 2024

Last updated on

May 13, 2026

Many parents in Canada wonder whether tuition fees paid to a registered charity — such as a private religious school — can be claimed as charitable donations on their tax return. As of 2026, the Canada Revenue Agency (CRA) position remains clear: in most cases, they cannot.

Tuition fees are payments for a service received, which disqualifies them from being treated as charitable donations under the Income Tax Act. This means official donation receipts typically cannot be issued for standard tuition payments.

There are exceptions — primarily for schools that provide religious instruction. A portion of fees tied strictly to religious education may qualify, but only if the school follows precise cost-segregation and receipting rules under CRA's Information Circular IC 75-23.

Understanding how these rules apply can help families know when they might claim a tax credit for part of their tuition fees, and help schools avoid costly receipting errors that put their charitable registration at risk.

What Does the CRA Say About Tuition and Charitable Donations? (IC 75-23 Explained)

The CRA's primary guidance on this issue is Information Circular IC 75-23: Tuition Fees and Charitable Donations Paid to Privately Supported Secular and Religious Schools. This document, which remains in effect in 2026, sets out the rules that determine when — and to what extent — tuition fees may be treated as a charitable donation.

IC 75-23 establishes three scenarios:

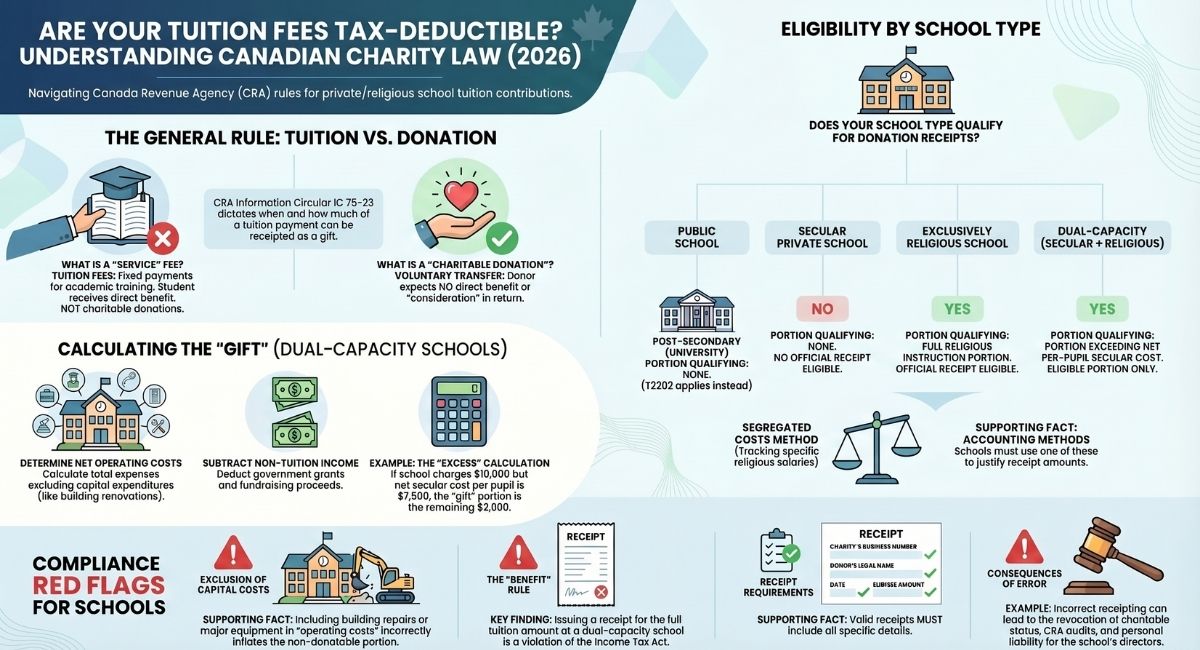

Scenario 1 — Purely secular private school: No portion of tuition qualifies as a charitable donation. The school is providing an academic service, and the CRA treats the full payment as tuition. No donation receipt can be issued.

Scenario 2 — Exclusively religious school: The full tuition payment related to religious instruction may be treated as a charitable donation. The CRA does not consider religious instruction to be a "service" in the same way academic education is. The school must be a registered charity and issue a proper official donation receipt.

Scenario 3 — Dual-capacity school (secular + religious): Only the portion of tuition that exceeds the school's net per-pupil cost for secular education qualifies as a charitable donation. The school must use either the Segregated Costs Method or the Cost Per Pupil Method — both explained further below — to calculate this amount accurately.

When Can Tuition Fees Qualify as a Charitable Donation? — At a Glance

Overview of Tuition Fees, Charities, and Tax Law

Payments made to schools can have different tax implications depending on whether they are considered tuition fees or charitable donations.

The distinction matters because the Income Tax Act treats these payments differently, especially when the school is a registered Canadian charitable organization.

The Canada Revenue Agency sets guidelines that help determine how these payments should be reported for tax purposes.

Defining Tuition Fees and Charitable Donations

Tuition fees are payments made in exchange for academic training.

These fees are typically fixed and cover the costs of providing education.

Because the student receives a direct benefit—the education—tuition fees are generally not classified as charitable donations.

A charitable donation is a voluntary transfer of money or property without expecting a direct benefit in return.

If a payment is made purely to support religious activities or a charitable cause, it may qualify as a donation eligible for a tax receipt.

Payments for standard academic tuition do not count as charitable donations under the Income Tax Act.

Only specific types of schools or circumstances may allow fees to be partially or fully treated as donations.

Role of Registered Canadian Charitable Organizations

A registered Canadian charitable organization must exist for charitable purposes and devote most of its resources to charitable activities.

These organizations can issue official donation receipts for gifts that support their work, according to the Income Tax Act.

Some religious schools operate solely for religious advancement.

If such a school is a registered charity, payments to it may be considered donations because they support its religious mission rather than academic training.

Schools providing both secular and religious education may issue donation receipts for the portion of fees that exceed the cost of academic tuition.

They must carefully track and separate their costs for secular and religious programs to do this.

Relevant Provisions in the Income Tax Act and Canada Revenue Agency Policies

The Income Tax Act outlines conditions under which tuition fees can be deducted or considered donations.

Section 60(f) allows deductions for tuition paid to designated educational institutions, but these deductions are not the same as charitable donation credits.

The Canada Revenue Agency’s Information Circular 75-23 clarifies that tuition fees paid to post-secondary or designated institutions are not charitable donations.

For private schools, donation receipts can be issued only when the school teaches exclusively religion or when fees exceed the cost of academic education in schools providing both religious and secular programs.

Schools must base donation calculations on their accounting records, excluding capital expenses and depreciation.

This ensures that only genuine support beyond academic costs qualifies for a charitable donation receipt.

General Rule on Tuition Fees as Charitable Donations

Payments made to schools are treated differently depending on whether they are considered tuition fees or voluntary contributions.

The presence of a direct benefit or service in return plays a key role in this assessment.

Tuition Payments Versus Voluntary Contributions

Tuition fees are amounts paid for academic instruction or services provided by a school.

These payments are generally not considered charitable donations.

Tuition represents compensation for education received, which is a clear benefit to the payer or their child.

Voluntary contributions differ in that they are given without expecting any specific service or benefit.

Only voluntary contributions may qualify as charitable donations if there is no direct exchange of goods or services.

If a school operates solely by donations and offers no formal tuition, those payments are more likely considered gifts.

The Income Tax Act specifically excludes tuition fees from donation eligibility.

It recognizes tuition as a form of payment for education, not a gift.

Criteria for Qualifying as a Charitable Donation

A payment must be a voluntary transfer of property made without consideration to qualify as a charitable donation.

The term "consideration" means that the donor does not receive anything of equivalent value in return.

For schools, a key criterion is whether the payment represents a donation or fee.

If the payment is for academic tuition, it is usually disqualified.

Donations are recognised when funds are given to support the school’s operation without receiving direct benefits, or for religious education provided by certain registered charities.

Only schools registered as Canadian charitable organizations may issue official donation receipts that support a tax credit claim.

Consideration and Benefit Assessment

Consideration refers to the benefit a payer receives in exchange for their payment.

If the payment provides tangible academic training or other services, it counts as consideration and the amount cannot be a charitable donation.

Payments to schools for religious instruction alone may avoid this consideration since religious education is not seen as a tangible service in the same way academic tuition is.

If a school combines secular and religious education, receipts may be issued only for the portion of payment that exceeds the calculated cost related to secular instruction.

This requires detailed accounting by the school to separate operating costs.

When a payment benefits the payer or their child directly, it usually disqualifies that payment from being a charitable donation for income tax purposes.

Exceptions: Religious and Dual-Capacity Schools

Certain tuition payments to registered charities may qualify as charitable donations, mainly when related to religious education.

The rules differ depending on whether the school provides exclusively religious instruction or a mix of religious and secular teaching.

Specific methods exist to determine the exact portion eligible for a donation receipt.

Exclusively Religious Schools

Tuition fees paid to schools that offer only religious education can partly be considered charitable donations.

These schools focus solely on religious training, such as teaching beliefs, practices, and history of a faith.

The Canada Revenue Agency (CRA) treats religious instruction as not involving a direct exchange of services, unlike standard tuition fees.

This means part of the tuition can be seen as a voluntary gift to the charitable work of the religious organisation running the school.

Only fees related to religious education qualify.

Payments for secular subjects, room, board, or other services do not count.

Parents or guardians paying tuition to such schools may claim a tax credit for the charitable donation portion.

Secular and Religious (Dual-Capacity) Schools

Schools teaching both secular and religious subjects are known as dual-capacity schools.

They provide regular academic subjects like math or science alongside religious education.

Only the portion of tuition related to religious instruction may be treated as a charitable donation.

The secular education part is seen as a service and is not eligible.

To qualify, the school must be a registered Canadian charitable organisation and clearly separate the costs of religious and secular education.

This separation ensures only the religious portion receives tax credit treatment.

Calculating the Charitable Donation Portion

There are two main ways to determine the charitable donation amount from tuition fees in religious or dual-capacity schools:

- Segregated Costs Method: The school tracks and separates expenses related to religious education, such as specific teacher salaries and supplies.

Only these costs count towards the donation portion. - Cost Per Pupil Method: Used when costs aren’t separated.

The school issues a receipt for the amount of tuition paid beyond the net operating cost per pupil for the whole school.

This excess represents the charitable portion.

Capital expenditures, like building repairs, are excluded from these calculations.

If a family has more than one child attending, each child’s tuition donation portion is considered separately.

📌 Practical Example (2026):

A dual-capacity school charges $10,000 per year in tuition. After accounting for government grants and other income, the school's net operating cost per pupil for the secular portion of education is $7,500. The remaining $2,500 represents the eligible charitable donation amount. The school may issue an official donation receipt for $2,500 only — not for the full $10,000.

Note: Capital expenditures such as building renovations must be excluded from the per-pupil cost calculation. Government grants and fundraising income must also be deducted from operating costs before the figure is used.

Accounting for School Fees, Operating Costs, and Tax Receipts

School fees contribute to the overall finances of educational institutions.

Understanding how operating costs and other income affect tax receipts is essential.

Accurate calculations ensure proper allocation of fees and clear eligibility for charitable donation claims.

Determining Net Operating Costs and Cost per Pupil

Net operating costs are the expenses directly related to running the school, excluding any capital expenditures or unrelated costs.

These include salaries, utilities, instructional materials, and maintenance.

Calculating the cost per pupil involves dividing the net operating costs by the total number of students enrolled.

This figure reflects the average expense to educate each student, which is critical for determining the non-donatable portion of fees.

Parents might receive receipts for the portion of tuition fees that exceed this cost per pupil, under certain charitable donation rules.

This requires precise and transparent financial records to support the amounts claimed.

Segregating Secular and Religious Education Costs

Schools offering both religious and secular education must separate these expenses clearly.

Religious instruction costs typically include wages for religious teachers, curriculum materials, and administrative costs tied solely to religious activities.

This segregation allows the school to identify which portion of fees qualifies for charitable donation receipts.

If costs are mixed, donations cannot be accurately calculated nor issued.

Records must include separate payroll accounts and detailed expense tracking for religious programming.

This ensures compliance with tax authority guidelines.

Exclusion of Capital Expenditures from Calculations

Capital expenditures cover long-term investments such as buildings, renovations, and major equipment purchases.

These costs do not count towards operating expenses when calculating the donation-eligible portion of tuition fees.

Only ongoing costs directly involved in delivering education are included in net operating costs.

Including capital costs would inflate operating expenses, reducing the donation-eligible amount and causing accounting inaccuracies.

Schools should record capital expenditures separately to maintain clear and accurate financial statements.

This ensures compliance with tax rules.

Role of Grants and Miscellaneous Income

Grants and miscellaneous income, such as government funding or fundraising proceeds, reduce the net operating costs the school must cover with tuition fees.

These funds lower the actual expenses borne by families, which affects the calculation of the cost per pupil.

Schools must accurately report any grants or other income to reflect the true financial picture.

Failure to account for these income sources can lead to overstated costs and incorrect tax receipts.

Transparent bookkeeping captures all income sources, contributing to fair and lawful issuance of donation receipts.

Tax Receipting Requirements and Compliance

Registered charities must follow strict rules when issuing official donation receipts for school tuition fees.

These rules ensure receipts are valid for taxation purposes and prevent misuse.

Understanding fair market value and how to handle split receipting is essential.

Non-compliance carries significant risks and penalties.

Official Donation Receipts: Required Information

An official donation receipt must include key information to be valid for tax purposes.

It should show the charity’s name, registration number, and the donor’s full name and address.

The receipt must specify the date of the donation and the amount given.

Receipts for tuition fees must clearly state the eligible amount considered a donation, excluding any part covering tuition or goods.

The receipt should be signed by an authorized representative of the charity.

Without all required details, the receipt cannot be used for claiming tax credits.

Fair Market Value and Split Receipting

Fair market value (FMV) is the price of any benefit a donor receives in return for their payment.

If a donor receives a benefit, like tuition services, the charity must subtract this FMV from the total payment before issuing a tax receipt.

Split receipting means separating the donation portion from the payment.

If a tuition fee includes a voluntary donation, the charity must issue a receipt only for that gift portion.

This system prevents donors from claiming tax credits on full tuition payments, which are not charitable donations.

Risks and Penalties for Non-Compliance

Charities that fail to follow donation receipting rules risk losing their privilege to issue official donation receipts.

They may face audits, fines, or legal challenges from tax authorities.

Directors of charities can be held personally liable if they allow improper receipting.

Incorrect receipting can lead to donors being denied tax credits, causing complaints and damage to the charity’s reputation.

Maintaining compliance protects both the charity and its donors from financial and legal consequences.

Common Mistakes Schools Make When Receipting Tuition as Donations

Even well-intentioned schools can make receipting errors that put their charitable registration at risk. Here are the most common mistakes to avoid in 2026:

1. Issuing receipts for the full tuition at a dual-capacity school. Unless the school is exclusively religious, only the portion above the per-pupil secular education cost qualifies for a donation receipt. Issuing receipts for the full tuition amount is a receipting violation under the Income Tax Act.

2. Failing to exclude capital costs from the per-pupil calculation. Capital expenditures like building renovations must be excluded from the operating cost used to determine the eligible donation amount. Including them inflates the calculation and results in receipts being issued for amounts that do not qualify.

3. Not deducting grants and government funding. Any government grants or fundraising income that offsets the school's operating costs must be deducted before calculating the per-pupil cost. Failing to do so overstates the eligible donation amount, which is a CRA compliance issue.

4. Issuing receipts without all required CRA information. A valid official donation receipt must include the charity's Business Number (BN), the donor's full legal name and address, the date of donation, and the precise eligible amount. Incomplete receipts cannot be used by donors to claim tax credits and may trigger a CRA review.

5. Assuming that registered charity status alone is enough. A school being a registered charity does not automatically mean its tuition payments qualify for donation receipts. Both the nature of instruction and CRA's receipting rules under IC 75-23 must be satisfied before any receipt is issued.

Schools and their administrators should seek legal advice before issuing tuition-related donation receipts for the first time or after any change in their programming or cost structure.

Additional Considerations for Educational Institutions in Canada

Educational institutions in Canada must navigate specific rules when it comes to tuition fees and charitable donations.

These include distinctions based on the type of institution, compliance with provincial education laws, and federal regulations influencing eligibility and reporting.

Eligibility of Post-Secondary and Designated Educational Institutions

Post-secondary institutions, such as universities and colleges, hold a distinct status. To qualify for tuition fee deductions, these institutions must be recognized as designated educational institutions under the Income Tax Act.

This includes those certified by provincial authorities or designated under the Canada Student Loans Act. Students attending these institutions receive official tax forms, like the T2202, that document eligible tuition fees.

Fees paid to designated institutions are deductible for tax purposes as educational expenses. These fees are not considered charitable donations.

Taxpayers should note that fees paid to post-secondary institutions cannot be treated as charitable donations, even if the institution is a registered charity.

Interaction with Provincial Educational Authorities and Legislation

Provincial educational authorities oversee private and public schools, including those that operate in both secular and religious capacities. These bodies ensure compliance with the School Act and related provincial legislation.

Schools must follow provincial guidelines for curriculum and operational standards. These standards affect how fees can be classified.

In some cases, a school needs provincial inspection or certification for its fees to qualify for special tax treatment. Schools that do not separate religious from secular education must carefully account for fees.

This accounting helps determine what portion may qualify as charitable donations under federal tax rules.

Canada Student Loans Act and Related Regulations

The Canada Student Loans Act defines designated educational institutions eligible for federal student aid programs. Institutions recognized under this Act include universities, colleges, and certain career programs.

Designation under the Act can impact an institution’s eligibility to issue official tax documentation for tuition fees. It may also influence student loan eligibility.

Only institutions meeting these federal standards can confirm their students’ fees as eligible for tuition tax credits. This maintains consistent rules across provinces.

Recognition under the Act also supports clarity in tax matters. This ensures educational payments align with federal program requirements.

Conclusion

As of 2026, the rules governing tuition fees and charitable donations in Canada remain unchanged under the Income Tax Act and CRA's IC 75-23 guidance. Tuition fees paid to a registered charity are generally not considered charitable donations because a service or benefit is received in exchange. Exceptions exist for parochial schools offering religious instruction, where a portion of the tuition may qualify as a donation — but only if costs are properly separated and calculated using CRA-approved methods.

The consequences for non-compliance have become increasingly significant as CRA continues to scrutinise registered charities. Schools and religious organisations that issue donation receipts for tuition should ensure their practices are reviewed regularly by a qualified charity lawyer.

At B.I.G. Charity Law Group, we can provide expert advice tailored to your specific situation involving tuition fees and charitable donations.

Reach out via email at dov.goldberg@charitylawgroup.ca or call us at 416-488-5888 to learn more. If you're interested, you can schedule a free consultation at CharityLawGroup.ca.

Our expert guidance ensures compliance with the Income Tax Act and helps families maximize eligible benefits.

Frequently Asked Questions

Payments for tuition fees to private schools are generally not eligible for charitable donation tax credits because they involve a direct exchange of services. However, specific rules apply to schools offering religious education and registered charities, which can affect how payments are classified and claimed.

Are tuition payments to private schools eligible for a charitable donation tax credit?

Tuition fees paid to private schools are usually not eligible for a charitable donation tax credit. Tuition is considered a payment for education services, not a voluntary gift.

How does the Canada Revenue Agency classify tuition fees for donation purposes?

The Canada Revenue Agency (CRA) does not consider tuition fees as charitable donations since there is an expected service in return. An exception exists for parochial or religious schools where part of the tuition may be seen as a gift.

What qualifies as a charitable donation?

A charitable donation is a voluntary transfer of money or property without expecting any goods or services in exchange. Payments that involve receiving a service, like tuition, do not qualify as donations.

Can a portion of tuition fees be claimed as a charitable donation if a school is a registered non-profit?

Yes, if the school provides religious instruction and is a registered charity, a portion of the tuition fees related to that religious education may be claimed as a charitable donation. Fees for non-religious education or extra services do not qualify.

What documentation is required to substantiate a charitable donation for tuition fees in Canada?

Official donation receipts issued by the registered charity are needed to claim a charitable donation. These receipts must clearly show the portion of the tuition that qualifies as a gift.

Are there exceptions that allow educational fees to qualify as charitable donations under the Income Tax Act?

Yes, the Income Tax Act allows exceptions for schools that offer only religious education.

In these cases, tuition payments for religious instruction may qualify as charitable donations.

Proper cost calculation methods and documentation are required.

Can a Jewish day school, Catholic school, or other faith-based school issue donation receipts for tuition?

Yes — if the school is a registered charity and provides religious instruction, it may issue official donation receipts. For schools that combine religious and secular education, only the portion of tuition exceeding the per-pupil cost of secular education qualifies. The school must calculate this amount using CRA-approved methods under IC 75-23, and receipts must meet all standard requirements for official donation receipts.

What happens if a school issues incorrect donation receipts for tuition?

If a registered charity issues donation receipts for amounts that do not qualify — for example, issuing receipts for the full tuition at a dual-capacity school — it risks losing its charitable registration, facing CRA audits, and having its donors' tax credits denied. Directors can be held personally liable in serious cases. Schools should obtain independent legal advice before issuing any tuition-related donation receipts.

Is the tuition tax credit the same as a charitable donation tax credit in Canada?

No — these are two entirely separate credits. The tuition tax credit (claimed using the T2202 form on Schedule 11) applies to eligible tuition at designated post-secondary institutions and is claimed by the student or transferred to a supporting individual. A charitable donation tax credit applies to voluntary gifts to registered charities and is claimed by the donor. The two credits cannot be combined for the same payment.

Has the CRA updated its position on tuition and charitable donations for 2026?

As of 2026, CRA's position under IC 75-23 remains unchanged. Tuition fees for secular education do not qualify as charitable donations, and the exceptions for religious schools continue to apply as previously set out. Charities and schools should continue to monitor the CRA website for any updates to this guidance and ensure their receipting practices reflect current requirements.

The material provided on this website is for information purposes only.. You should not act or abstain from acting based upon such information without first consulting a Charity Lawyer. We do not warrant the accuracy or completeness of any information on this site. E-mail contact with anyone at B.I.G. Charity Law Group Professional Corporation is not intended to create, and receipt will not constitute, a solicitor-client relationship. Solicitor client relationship will only be created after we have reviewed your case or particulars, decided to accept your case and entered into a written retainer agreement or retainer letter with you.

DOV GOLDBERG, J.D. is a lawyer at B.I.G. Charity Law Group and has dedicated his career exclusively to Charity and Not-for-Profit Law for over a decade. Dov guides charities, foundations, and non-profit organizations through every stage of the registration process, offering practical legal advice with a focus on compliance, governance, and long-term success. Known for his hands-on approach and deep knowledge of CRA requirements, Dov is committed to helping clients build strong, sustainable, and legally sound organizations.

.png)